Regulated vs. Unregulated Brokers: Why It Matters

Learn the crucial differences between regulated and unregulated brokers, the risks involved, and how to choose the right broker for secure and transparent trading.

Writen by:

Arslan Ali But

07 January 2025

8 minutes read

Writen by:

Arslan Ali But

07 January 2025

8 minutes read

Writen by:

Arslan Ali But

07 January 2025

8 minutes read

Choosing the right broker is one of the most critical decisions a trader can make. Ever wondered if your broker is truly safeguarding your funds? Brokers act as the gateway to financial markets, and their practices can directly impact your trading experience and fund safety. Broadly, brokers fall into two categories: regulated and unregulated.

Regulated brokers operate under strict guidelines set by reputable financial authorities, ensuring transparency, fair practices, and client fund protection. In contrast, unregulated brokers lack oversight, increasing the risk of fund misuse, hidden fees, and difficulties with withdrawals.

The difference between these two types of brokers is stark. While regulated brokers prioritize your safety, unregulated ones may prioritize their profit—often at your expense.

This article explores the distinctions between regulated and unregulated brokers, shedding light on the risks involved and the importance of choosing a regulated broker for secure and reliable trading.

What Are Regulated Brokers?

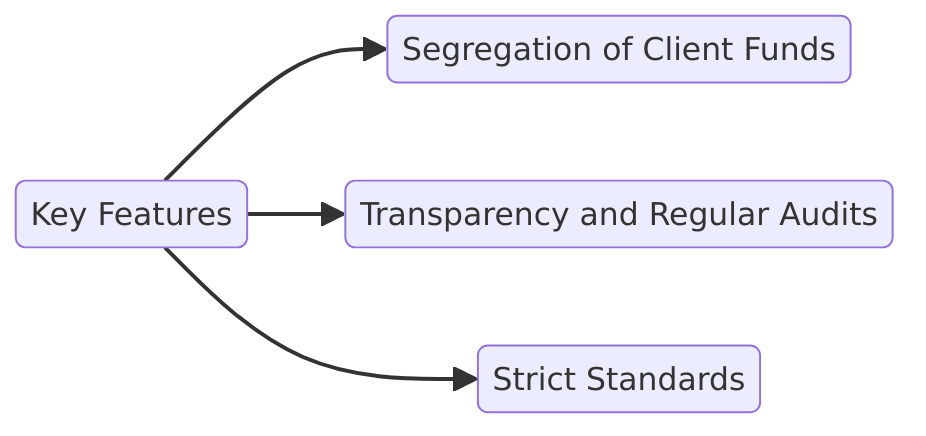

Regulated brokers are financial institutions licensed and monitored by recognized authorities such as the FCA (UK), ASIC (Australia), CySEC (EU), or CFTC (US). These brokers follow strict rules to ensure transparency and protect client funds.

Key Features:

- Segregation of Client Funds: Regulated brokers must hold client funds in separate accounts, ensuring they are not used for operational purposes. For example, the FCA requires brokers to segregate funds, providing protection for amounts up to £85,000 under the FSCS scheme.

- Transparency and Regular Audits: Brokers are subject to frequent audits and must disclose financial data. 95% of FCA-regulated brokers publish annual reports, fostering trader confidence.

- Strict Standards: Authorities like ASIC enforce leverage limits (e.g., 30:1 for retail clients) to reduce excessive risk.

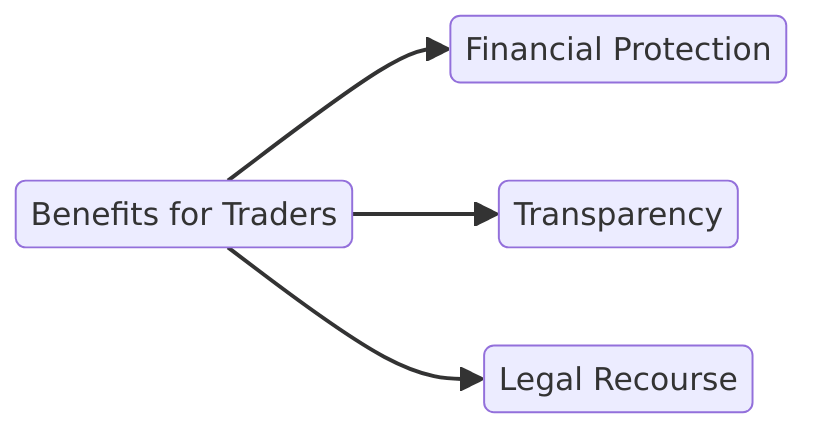

Benefits for Traders:

- Financial Protection: Regulatory bodies often mandate capital reserves. For instance, the CFTC requires brokers to maintain a minimum net capital of $20 million, reducing insolvency risks.

- Transparency: Around 90% of traders prefer brokers offering clear terms on fees and conditions, according to industry surveys.

- Legal Recourse: Compensation schemes like CySEC’s ICF protect up to €20,000 per client, ensuring trader claims in case of disputes.

Engaging with regulated brokers ensures a safer trading environment with accountability and trust.

Unregulated Brokers: Understanding the Risks

Unregulated brokers operate without oversight from recognized financial authorities such as the FCA, ASIC, or CySEC. This lack of monitoring allows them to bypass industry standards, creating significant risks for traders.

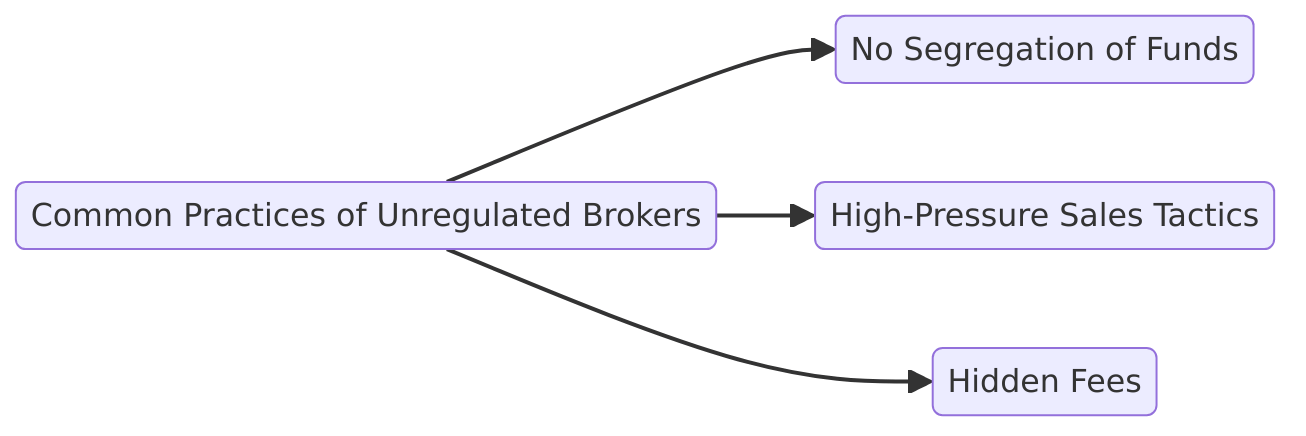

Common Practices of Unregulated Brokers:

- No Segregation of Funds: Unlike regulated brokers, unregulated brokers often mix client funds with their operational accounts, increasing the risk of fund misuse.

- High-Pressure Sales Tactics: They may use aggressive marketing strategies to lure traders into making deposits quickly, often with promises of guaranteed profits.

- Hidden Fees: Unregulated brokers frequently impose unexpected charges, such as inflated withdrawal fees or overnight holding costs.

Risks Involved:

- Fund Misuse: Without segregation rules, your deposits may be used for the broker’s operations or speculative activities.

- Difficulty Withdrawing Funds: Many traders report delays or outright refusal when attempting to withdraw their money.

- Lack of Accountability: With no regulatory body to oversee their practices, traders have little to no recourse in case of disputes.

Key Differences Between Regulated and Unregulated Brokers

Understanding the differences between regulated and unregulated brokers is essential to safeguard your investments. Here’s a breakdown with examples and relevant figures:

-

Fund Security

-

Regulated Brokers: Brokers like eToro are required to

maintain segregated accounts, ensuring client funds are separate from operational funds. This

protects traders’ money in case of insolvency.

- Example: The FCA (UK) mandates segregated accounts, and under the FSCS, clients are insured up to £85,000.

- Unregulated Brokers: Without segregation, funds can be used for the broker’s operations. According to industry reports, over 70% of complaints against unregulated brokers involve fund misuse or withdrawal delays.

-

Regulated Brokers: Brokers like eToro are required to

maintain segregated accounts, ensuring client funds are separate from operational funds. This

protects traders’ money in case of insolvency.

-

Transparency

- Regulated Brokers: Regular audits ensure accountability. For instance, ASIC (Australia) enforces strict financial reporting, and 95% of its regulated brokers publish annual transparency reports.

- Unregulated Brokers: Lack oversight, leading to opaque practices like hidden fees or manipulated prices. Studies show most fraud cases in forex trading involve unregulated brokers.

-

Dispute Resolution

-

Regulated Brokers: Offer legal recourse through regulatory

bodies. Traders can escalate disputes via organizations like CySEC or the CFTC.

- Example: The CFTC reported resolving disputes totaling $120 million in client recoveries in 2023.

- Unregulated Brokers: With no regulatory body, traders have less than 20% success in recovering funds from disputes.

-

Regulated Brokers: Offer legal recourse through regulatory

bodies. Traders can escalate disputes via organizations like CySEC or the CFTC.

-

Compensation Schemes

-

Regulated Brokers: Provide financial protection.

- Examples:

- FSCS (UK): Covers up to £85,000.

- ICF (EU): Compensates clients up to €20,000.

- Unregulated Brokers: No compensation mechanisms exist, leaving clients vulnerable in case of broker failure.

-

Regulated Brokers: Provide financial protection.

Red Flags to Spot an Unregulated Broker

Identifying unregulated brokers early is essential to protect your investments. Here are the key warning signs to watch out for:

-

Unrealistic Promises

Unregulated brokers often lure traders with guarantees of high returns and minimal risk—claims that no reputable broker would make. For instance, promises like “Earn 100% in a week” should raise immediate concerns.

-

Absence of Verifiable Licensing Details

A lack of regulatory credentials is a major red flag. Regulated brokers typically display their licensing information prominently, including their registration number and the regulatory authority. Unregulated brokers often evade questions or provide unverifiable details.

-

Poor or No Customer Support

Unregulated brokers may have unresponsive or nonexistent customer service. Difficulty reaching support for queries or withdrawals is a common complaint among traders dealing with such entities.

-

Unclear Terms and Conditions

Hidden fees, vague withdrawal policies, or overly complex terms are telltale signs of an unregulated broker. These tactics often lead to disputes or loss of funds.

Importance of Verification

Always verify a broker’s regulatory credentials through official databases like the FCA (UK), ASIC (Australia), or CySEC (EU). Cross-check their registration number to ensure legitimacy.

Why Regulation Protects Traders

Regulation is essential for protecting traders and ensuring a secure trading environment.

Provides a Safety Net: Regulated brokers must segregate client funds from their operational accounts, ensuring your money is protected even if the broker faces insolvency.

Compensation schemes like:

- FSCS (UK) cover up to £85,000

- ICF (EU) provides up to €20,000

Additionally, negative balance protection prevents traders from losing more than their initial deposit.

Encourages Fair Trading Practices: Regulatory oversight enforces transparency and accountability, requiring brokers to publish financial reports and undergo regular audits. This ensures fair pricing and minimizes the risk of manipulation.

Builds Trust: Regulated brokers adhere to high ethical standards set by authorities like the FCA, ASIC, and CySEC, offering traders peace of mind and a reliable trading experience.

Choosing a regulated broker safeguards your investments and ensures fair and transparent trading.

How to Choose a Broker

Selecting the right broker is crucial for a safe trading journey. Follow these steps to ensure reliability:

- Verify Regulatory Credentials: Check if the broker is licensed by reputable authorities such as the FCA (UK), ASIC (Australia), or CySEC (EU). Verify their registration number through official databases.

- Research Reputation: Look for reviews on platforms like Trustpilot or ForexPeaceArmy. Pay attention to feedback on fund safety, withdrawals, and customer support.

- Understand Terms and Fees: Read the broker’s terms, focusing on withdrawal policies, commissions, and additional fees. Avoid brokers with unclear or overly restrictive conditions.

- Utilize Verification Resources: Use tools like regulatory body websites to confirm legitimacy and avoid unregulated brokers.

By taking these steps, you can ensure your broker meets high safety and transparency standards.

Conclusion

Trading with regulated brokers is non-negotiable for securing your investments. They provide essential protections like segregated accounts, transparency, and compensation schemes, minimizing risks and ensuring fair trading practices.

Unregulated brokers, on the other hand, expose traders to fund misuse, withdrawal issues, and lack of accountability. Always verify a broker’s credentials, regulatory status, and reputation before trusting them with your money.

Final Advice: Don’t risk your hard-earned capital on unregulated brokers. At WhereToTrade, we’re committed to guiding you in choosing a trusted, regulated broker to trade with confidence.

Table of contents

1. What Are Regulated Brokers? 2. Unregulated Brokers: Understanding the Risks 3. Key Differences Between Regulated and Unregulated Brokers 4. Red Flags to Spot an Unregulated Broker 5. Why Regulation Protects Traders 6. How to Choose a Broker 7. Conclusion